Cash is king. You’ve heard it forever, but do you know what it really means?

Cash is king. You’ve heard it forever, but do you know what it really means?

Cash in this context isn’t bills or coins, it’s money in the bank that you can spend today. It’s the single most important resource in any business—your cash flow can make or break your business, but there’s a critical difference between cash and profits that is frequently misunderstood.

You need cash in the bank

The problem with cash in business is that we tend to take it for granted. We think in profits, but we spend cash. The issue is, profits and cash are different.

What are profits? Profits is an accounting concept that depends on a lot of imposed timing constraints for sales, costs, and expenses.

What is revenue? Revenue is money coming into the business. For most accounting and financial analysis purposes, it’s the same as sales. But technically, revenue can also include sales of assets and money coming in as loans and investments.

What is cash? Cash, on the other hand, is what it takes to pay your bills—the actual money you have in hand.

Although cash is critical, people think in profits instead of cash. We all do. When you imagine a new business, you think of what it would cost to make the product, what you could sell it for, and what the profits per unit might be. We are trained to think of business as sales minus costs and expenses, which is profits.

However, we don’t spend the profits in a business. We spend cash. Profitable companies go broke because they have all their money tied up in assets that can’t quickly be converted to cash, such as inventory money owed as accounts receivable from customers who haven’t paid old invoices.

Every dollar of money owed by customers in accounts receivable is a dollar that has been included in the sales and profits but isn’t available to pay bills. Every dollar of inventory is a dollar that looks good as an asset on the books but isn’t available to pay bills. In the meantime, despite those assets on the books, they don’t have enough money to pay their expenses. Working capital, meaning money in the bank or liquid investment, is critical to business health.

Unfortunately, we often don’t see the cash flow implications as clearly as we should, which is one of the best reasons for proper business planning. We have to manage cash as well as profits.

Sales on credit: Waiting to get paid

A business delivers the goods or services to a business customer or client along with an invoice. The check comes later. That’s extremely common in business-to-business sales, and what it means is that the amount of that invoice is included in the month’s sales, and is booked as sales—but it isn’t actually cash in the bank.

Instead, that amount sits in a bookkeeping category called accounts receivable until the check arrives and it’s deposited into the bank. The average time between delivering the invoice and receiving the money is called collection days, or collection period. The problem businesses face is that all the money in accounts receivable shows up in profits as sales, but is not in your bank account. You can’t spend it.

Profitable businesses can go under simply because they have too much money in accounts receivable, and not enough in the bank—they have trouble getting their invoices paid on time. The money showed up in sales but never made it to the bank. Ultimately, being profitable didn’t prevent business failure.

Inventory: Buying things before you sell them

Most product businesses, such as stores, have to buy the things they sell ahead of time before they sell them. Manufacturers and assemblers have to buy components and materials before they create and sell finished goods, and that creates a lot of potential cash flow problems.

It’s called inventory: products for resale, materials for manufacturing, components for assembly. Money spent on inventory doesn’t show up in profits until the ultimate sale—but it’s gone, out of the bank, when it’s spent.

For businesses that depend on inventory, inventory management can be critical for cash flow. It’s too easy to have money tied up in inventory that sits on the shelves too long, or never gets sold. That money is gone from the bank account but doesn’t show up in the profit and loss.

Bills: Money in the bank versus the money you owe

The opposite of accounts receivable is called accounts payable, which is money a business owes to its vendors.

Taking 30 or more days to pay invoices is good for your own cash flow. Every dollar you have sitting in accounts payable is a dollar that counts as expenses, and decreases profits, but is in fact still a dollar in your own bank. You own that dollar until you pay it out. You subtract expenses from profits when you incur them, not when you pay them.

So payables are the opposite of receivables: with receivables, your customers have your money; with payables, you have your vendors’ money.

The difference between cash and profits: A case study

To help illustrate the difference between cash and profits, here’s an example: Garrett’s Bike Shop, a bicycle store in a medium-sized local market, with sales of about $400,000 per year.

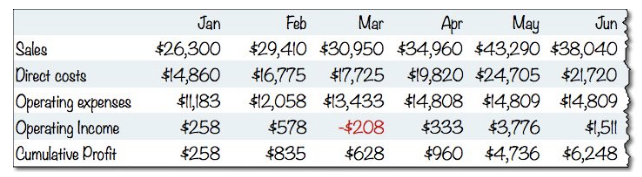

The first chart below shows key operating numbers for that store over a few months. You see sales, direct costs, expenses, and profits.

Now we compare that to a simple cash flow projection based on the assumption that the store makes 90 percent of its sales on account (to be paid later) and its customers wait two months to pay those invoices (that would be unusual for a bicycle store, yes, but it’s the common case for most existing business-to-business companies).

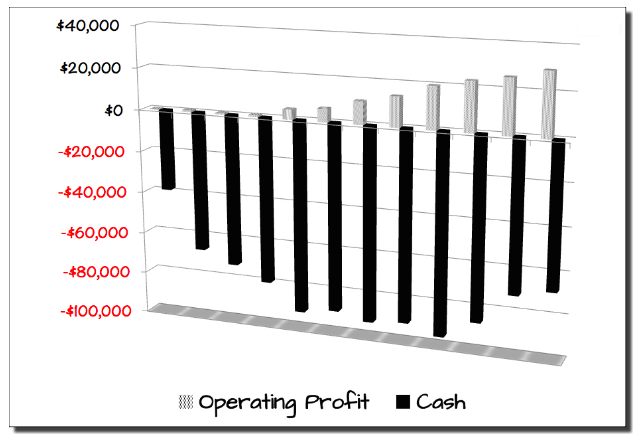

Also, let’s assume Garrett keeps about a month’s worth of sales as products in the store, called inventory, that customers can buy, and he has to buy those products in advance of selling them. The result is cash flow vastly different from profits, as you can see in the following illustration:

The difference between profits and cash, in this case, is more than $90,000 for a business selling about $30,000 monthly. That business would be profitable but bankrupt for lack of cash.

The change in the two scenarios is just cash flow, not a penny of sales, the cost of sales, or expenses. No prices are changed, no new employees added, and no changes made in salary.

Here’s what that difference looks like graphically:

The real bottom line: Mind the cash flow

The phrase “the bottom line” is a reference to profits, which are the bottom line of the profit and loss statement. But it’s actually come to mean something like a conclusion, or the most important result. That’s why the real bottom line for business owners is cash flow, not profits.

Profitable companies can run out of money due to lack of cash flow. There’s no way around it: To run a business, you have to mind cash flow, not just profits.

Editor’s note: This article was updated in 2018.

from Bplans Articles https://ift.tt/2qj2tJC

No comments:

Post a Comment