This article is part of our Restaurant Business Startup Guide—a curated list of articles to help you plan, start, and grow your restaurant business!

With restaurants, as with most businesses, there is no single right way to do a sales forecast. The best sales forecast method will vary according to how you manage information, how much past data you have access to, and what special factors drive your business. With this example, I want to show you one way that one person did it, so you can copy this method or use it to inspire your own method or this one with modifications.

For the case sample here, I’m looking at how Magda forecasts her sales for a café she wants to open in an office park. She wants a small locale, just six tables of four. She wants to serve coffee and lunches. She hasn’t contracted the locale yet, but she has a good idea of where she wants to locate it and what size she wants, so she wants to estimate realistic sales. She assumes a certain size and location and develops a base forecast to get started.

Establishing a base case

She starts with understanding her capacity. She does some simple math. She estimates that with six tables of four people each, she can do only about 24 sit-down lunches in an average day, because lunch is just a single hour. And then she adds to-go lunches, which she estimates will be about double the table lunches, so 48 per day. She estimates lunch beverages as .9 beverages for every lunch at the tables, and only .5 beverages for every to-go lunch.

Then she calculates the coffee capacity as a maximum of one customer every two minutes, or 30 customers per hour; and she estimates how she expects the flow during the morning hours, with a maximum 30 coffees during the 8 to 9 a.m. hour. She also estimates some coffees at lunch, based on three coffees for every 10 lunches. You can see the results here, as a quick worksheet for calculations.

Where do those estimates come from? How does Magda know? Ideally, she knows because she has experience. She’s familiar with the café business as a former worker, owner, or close connection. Or perhaps she has a partner, spouse, friend, or even a consultant who can make educated guesses. And it helps to break the estimates down into smaller pieces, as you can see Magda has done here.

And, by the way, there is a lesson here about estimating and educated guesses: Magda calculates 97.2 coffees per day. That’s really 100. Always round your educated guesses. Exact numbers give a false sense of certainty.

She then estimates monthly capacity. Look at the above illustration and you’ll see that she estimates 22 workdays per month, and multiplies coffees, lunches, and beverages, to generate the estimated unit numbers for a baseline sample month.

So that means the base case is about 1,500 lunches, about 1,000 beverages, and about 2,000 coffees in a month. Before she takes the next step, Magda adds up some numbers to see whether she should just abandon her idea. At $10 per lunch and $2 per coffee or beverage, that’s roughly $15,000 in lunches, $2,000 in lunch beverages, and $4,000 in coffees in a month. She probably calls that $20,000 as a rough estimate of a true full capacity.

She could figure on a few thousand in rent, a few thousand in salaries, and then decide that she should continue planning, from the quick view, like it could be a viable business. (And that, by the way, in a single paragraph, is a break-even analysis.)

From base case to sales forecast

With those rough numbers established as capacity, and some logic for what drives sales, and how the new business might gear up, Magda then does a quick calculation of how she might realistically expect sales to go, compared to capacity, during her first year:

Month-by-month estimates for the first year

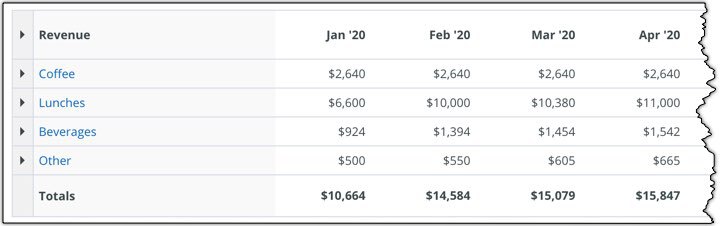

From there, it’s using a simple model, like a spreadsheet. She inputs the row definitions, unit sales estimates, average prices, and average direct costs to create a complete sales forecast. The first illustration here shows the table results for sales for the first few months. The numbers come from multiplying projected unit sales times projected average price per unit.

These are all based on Magda’s calculations above, with an additional row added for “other,” which is t-shirts and mugs and such.

And this illustration from LivePlan (you can do this on a simple DIY spreadsheet as well) shows the data input for unit sales of lunches, one of the four rows of sales. Compare the ups and downs of these estimated unit sales to the capacity estimates above; you can see, visually, that they are related. No need, however, to go into the details; that might make it seem more scientific than it really is.

I’m not including an illustration here of price assumptions. They are simple estimated averages over the entire business. Magda estimates lunches at $10 each, coffee at $2 each, and beverages also at $2 each. These are general guesses, based on experience.

Furthermore, you can see here throughout, how she’s working with educated guessing. She isn’t turning to some magic information source to find out what her sales will be. She doesn’t assume there is some magic “right answer.” She isn’t using quadratic equations and she doesn’t need an advanced degree in calculus. She does need to have some sense of what to realistically expect. In this case, she’s worked in a restaurant (or knows somebody who has), so she has some reasonable information to draw on.

The right level of detail

Notice here that Magda doesn’t try to break lunches down into sandwiches, soup, burgers, ham versus cheese, turkey versus beef, or any of that detail. Too much detail doesn’t work well in the real world. Instead, she summarizes and aggregates enough to make a useful forecast that she can track, review, and revise as needed with the ongoing business.

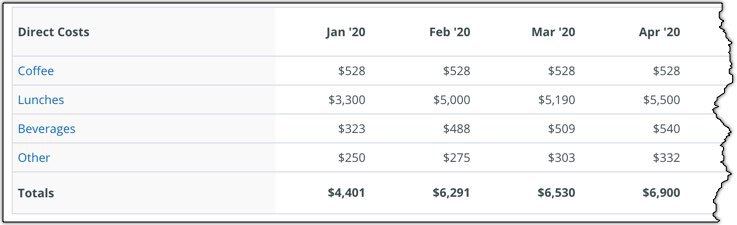

Estimating direct costs

Along with sales, it’s advisable to estimate direct costs, also called COGS, or cost of goods sold, or unit costs. These are costs that the business incurs only in delivering what it sells. In Magda’s case, it’s what she pays for the coffee beans, beverages, bread, meat, potatoes, and other ingredients in the food she serves. For a bookstore, it’s what the book paid for the books it sells. For a taxi business, it’s the gasoline and routine maintenance. Direct costs are useful for comparison basis.

So, with her unit sales estimates already there, Magda needs only add estimated direct costs per unit to finish the forecast. The math is as simple as it was for the sales, multiplying units times per-unit direct cost. Then it adds the rows and the columns appropriately. Here’s the finished example showing direct costs in a table. If you’re following along, Magda estimated per unit direct costs (not shown here) as 50 percent of the sales price for lunches, 20 percent of the coffees, and 35 percent of drinks.

So you can see illustrated here the idea of educated guessing, estimates, and summary. Here too, as with the sales above, Magda doesn’t break down all the possibilities for lunches into details, differentiating the steak sandwich from the veggie sandwich, and everything in between—that level of detail is unmanageable in a forecast.

She estimates the overall average direct cost. Coffees cost an average of 40 cents per coffee, and lunches about $5.00. She estimates because she’s familiar with the business. And if she weren’t familiar with the business, she’d find a partner who is, or do a lot more research.

from Bplans Articles https://ift.tt/2Jr6YOJ

No comments:

Post a Comment